We bring expertise in carbon markets, decarbonisation strategy, and value creation

Access our case studies

Enter your details to access our case studies and learn how MacGregor Advisory Group helps clients with:

- Demand-side challenges

- Marketplace Matchmaking

- Supply-side solutions

Thank you! We’ll be in touch soon.

Something went wrong while submitting.

Demand-side challenges

Our team has deep expertise assisting

Oil and Gas industry

Defining the strategic case for carbon market participation

Power sector

Strategic alignment to de-carbonise power section within an EU country

Climate

Global multi asset class asset manager

Green investment products

Determine exposure to future growth sectors and long-term value

DEEP DIVE

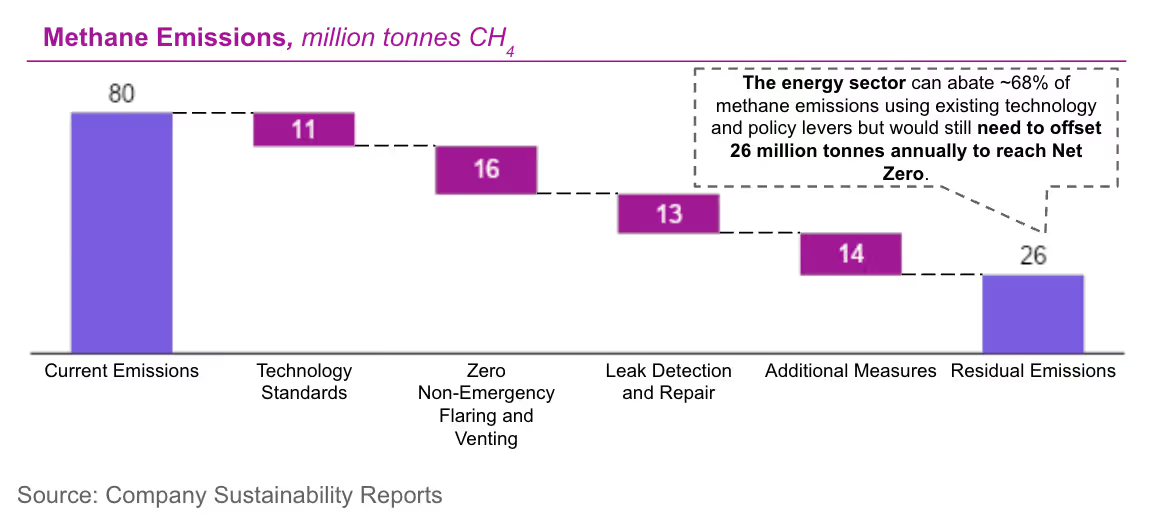

Oil & Gas industry

We advised the client on how to address methane emissions challenges in Oil & Gas and identified commercial options to monetise abatement and offsets

As part of our broader analysis, we identified Oil & Gas as the second-largest source of anthropogenic methane, primarily emitted during extraction.

Industry overview:

- Methane is emitted from Oil & Gas operations during production, representing one of the best near-term opportunities for climate action because the pathways for reducing them are well-known and cost-effective.

- Around 40% of oil and gas methane emissions could be reduced at no net cost using existing technologies (e.g. leak detection and repair campaigns, installing emissions control devices, etc.).

- After abatement projects are carried out, the key challenge in reaching Net Zero methane emissions is the residual hard-to-abate emissions.

- These emissions create a strong need for credits specifically reducing methane.

Three key factors drive the demand for methane reduction credits from Oil & Gas majors:

- Regulatory scrutiny on methane emissions

- Hard-to-abate residual emissions

- Continued demand for Oil & Gas in a Net Zero world

Supply-side solutions

Our team has deep expertise assisting

Nature Based Solutions

Carbon Credit (CORSIA / Singapore) Go-to-market strategy

.svg)

Chemical industry

Re-imagined operating model using bio-feedstock

Petrochemical industry

Operating Model transition and Value of Carbon for Corporate Capital

Carbon Inset asset transaction

Asset transaction including operational control to allow balance sheet insetting

Marketplace matchmaking

Our team has deep expertise assisting

Commercial strategy and carbon credits go-to-market

White paper

Analysis of Australian compliance hybrid and voluntary markets

Construction industry

Carbon market design and future trends

Carbon market buyer preferences

Different Carbon Credit products may preferentially fit some buyers/sectors

DEEP DIVE

White paper: Carbon market trajectory

We were engaged to develop a white paper on the evolving Australian carbon market and advise on its likely future trajectory

Among the depth of analysis we delivered, one of the most compelling insights was…

DEEP DIVE

Construction industry

We identified unmet demand for sustainable development in the construction sector in Australia and advised our client on how to unlock value through strategic sustainability

We discovered a strong demand for sustainable buildings in the APAC commercial sector in particular.

And then advised on emerging opportunities for developers to make meeting that demand more commercially viable.

DEEP DIVE

Carbon market buyer preferences

We performed buyer analysis for a decarbonisation solution provider to understand buyer preferences for carbon credits

Illustrative example of Carbon Market Buyer Preference analysis.